- sales growth of more than 16%

- EBITDA up by more than 50% (+32% excluding non-recurring items)

- Group share of net attributable income up by 75%

> Improved outlook for fy 2021/2022 as a whole

> Positive free cash flow forecast for fy 2021/2022

Paris, May 24, 2022 – The Board of Directors of Compagnie des Alpes, in a meeting chaired by Dominique Marcel, approved the Group’s consolidated financial statements for the 1st half of financial year 2021/2022.

Commenting on the results for the 1st half of 2021/2022, Dominique Thillaud, CEO of Compagnie des Alpes stated: «The results of the first half are very encouraging. They demonstrate an exceptional level of commitment by Compagnie des Alpes teams and the success of initiatives undertaken for the purpose of accelerating – over and above the market recovery – growth across the board for our business lines. Building on the good performances recorded last summer, the leisure parks had a very good first quarter, with the Halloween and Christmas periods, while the ski areas fully capitalized on the action taken in the field. The Group is ahead of its operating plan and should be able to surpass its pre-crisis level performances for the financial year 2021/2022.

Having recovered the resources needed to achieve our development and growth ambitions, we plan to maintain our investment efforts in attractivity, continue to deploy our digital tools, optimize our distribution channels and our sales strategy, while accelerating the rollout of our net zero carbon objectives, which remains essential for our businesses and for the regions in which we operate.”

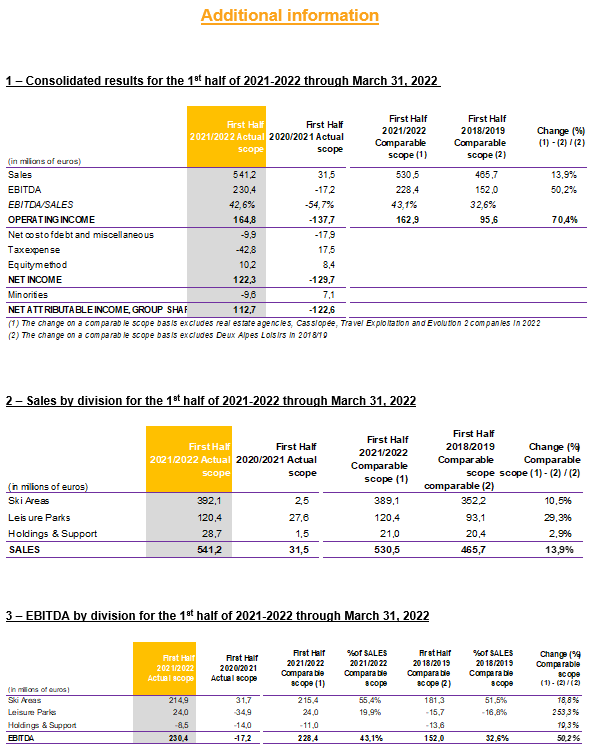

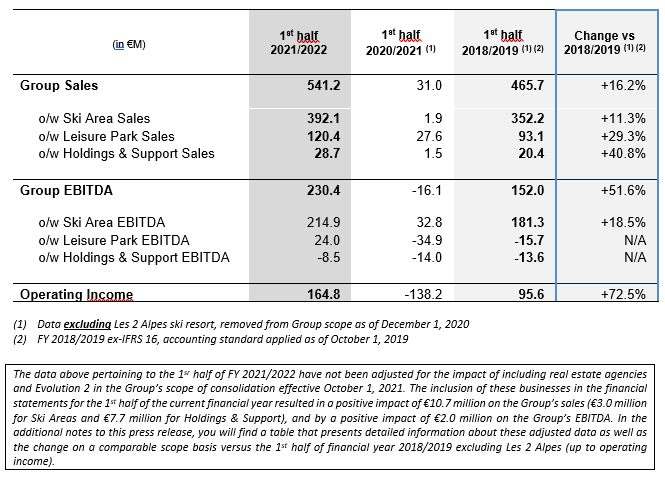

The Group’s Consolidated Sales for the 1st half of 2021/2022 amounted to €541.2 million, an increase of 16.2% compared with the 1st half of 2018/2019 (adjusted for the removal of Les 2 Alpes), the reference period because it is the most recent full year preceding the health crisis.

For Ski Areas, sales came to €392.1 million, which represents growth of 11.3% versus the 1st half of financial year 2018/2019. After having been impacted to the travel restrictions in effect between the United Kingdom and France until the end of January 2022, the number of skier days gradually made up for its performance gap compared to the 1st half of 2018/2019 as these restrictions were lifted, reflecting also good French school holiday performances in February and a slight improvement in the month of March.

Overall, the decline in the number of skier days was limited to -5% for the first half compared to the same period in 2018/2019. Average revenue per skier day rose by around 15% thanks to a less intermediated client mix, an improved package mix, and the aggregate addition of price indexing over the last three financial years.

For Leisure Parks, sales reached €120.4 million, which represents an increase of 29.3% compared with the 1st half of financial year 2018/2019. Reflecting the successful acceleration of event-focused marketing during the periods surrounding Halloween and Christmas, this performance was driven by an increase in attendance (+10%) and by the rise in spend per visitor (+19%), which remains highly dynamic. Both figures illustrate the relevance of new investments in attractivity, the digital development strategy, and the optimization of the sales strategy (yield management in particular) deployed by the Group to accelerate the recovery.

Holdings & Support sales totaled €28.7 million, an increase of 40.8% versus the 1st half of financial year 2018/2019, due to the consolidation of the Group’s real estate agencies since October 1, 2021. Adjusted for this consolidation, the increase in sales comes to just under 3% compared with the 1st half of 2018/2019. Travelfactory reported a satisfactory level of activity, not only in the French market but also in the United Kingdom, the Netherlands, and Belgium. In addition, the rollout of Travelski Express was a success, with a ramp-up that resulted in nearly fully booked rotations by the end of the period. Following this experiment – whose economic equilibrium was slightly impacted by a late start (caused by the closure of the UK market and the Omicron variant) – the Group plans to pursue the development of its sustainable mobility initiatives.

The Group’s EBITDA was €230.4 million for the 1st half of 2021/2022, up by 51.6% compared with EBITDA of €152.0 million for the 1st half of financial year 2018/2019 (adjusted for Les 2 Alpes). It got a boost from non-recurring positive items for a total of €29.1 million, including €19.8 million worth of insurance compensation related to the flooding that hit parts of Walibi Belgium and Aquilibi in July 2021, and €9.3 million in remaining financial aid and exemption from social charges in France and abroad relating to the health crisis in the first part of 2021. They also include the positive impact of applying IFRS 16, for €7.3 million (it should be noted that this standard was not applicable in 2018/2019).

EBITDA for Ski Areas reached €214.9 million (of which €2.4 million reflected the impact of applying IFRS 16), an increase of 18.5% compared with the 1st half of 2018/2019 adjusted for Les 2 Alpes. This performance is attributable to solid business dynamics during this period, as well as to disciplined management of operating expenses and the one-off impact of the reduction in social charges because of the health crisis, which was booked this half for €6.6 million.

EBITDA for Leisure Parks was +€24.0 million (including the €3.8 million impact of IFRS 16) versus €-15.7 million for the 1st half of 2018/2019. This performance can be attributed foremost to the very good level of sales for this division, particularly during the 1st quarter, as well as to disciplined management of operating costs. It also includes non-recurring positive items for a total of €21.1 million: +€19.8 million in net insurance compensation related to the flooding in Belgium that occurred in July 2021 and €2.2 million in subsidies linked to the health crisis that were recorded this financial year.

EBITDA for Holdings & Support also improved, reaching -€8.5 million (including the €1.0 million positive impact of applying IFRS 16), versus -€13.6 million for the 1st half of 2018/2019. This improvement is primarily due to a good level of business for tour operators and reflects the one-off positive impact of exemption from social charges payable at the holding level, for €0.5 million.

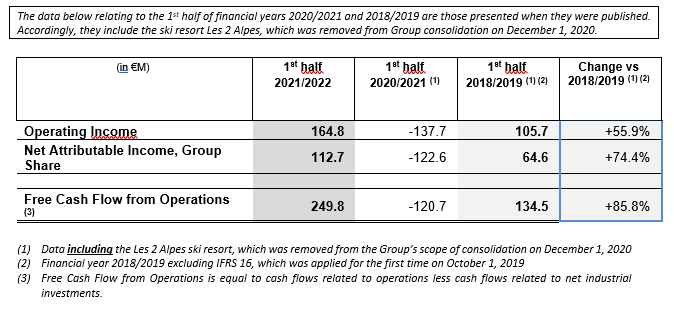

After factoring in Depreciation and amortization expense, which increased by close to €10 million versus the 1st half of 2018/2019, primarily due to the impact of IFRS 16 (€6 million), the Group’s operating income amounted to €164.8 million, an increase of 55.9% compared with the same period in financial year 2018/2019.

The Group’s net cost of debt was €8.0 million for the period under review, a marked decrease compared with the 1st half of the preceding financial year, which included a €4.3 million expense related to the extension of the first PGE loan. Compared with the 1st half of 2018/2019, net cost of debt increased due to the cost of PGE guarantee costs prorogated and IFRS16 financial costs expense (€1.9 million).

After recording a tax expense of -€42.8 million and results for companies accounted for using the equity method for +€10.2 million, Net attributable income, Group share for the 1st half of financial year 2021/2022 was €112.7 million, versus €64.6 million for the 1st half of 2018/2019, an increase of 74.4%.

The decrease in working capital requirements reached -€85.4 million. This is in line with the level of activity observed over the course of the 1st six months of the financial year and is due primarily to higher operating costs.

Net industrial investments reached €65.0 million during the 1st half, which represents a relatively low proportion of the annual budget due to a phasing plan that calls for higher outlay in the 2nd half. The total of €65.0 million breaks down into €31.5 million for Ski Areas, €27.3 million for Leisure Parks, and €6.3 million for Holdings & Support.

Free Cash Flow from Operations is thus up sharply, to €249.8 million versus €134.5 million for the 1st half of 2018/2019. It is nonetheless expected to decrease over the 2nd half of the year due to the seasonal nature of the change in WCR and the execution of investments.

After factoring in lease liabilities of €163.5 million (in accordance with IFRS 16), the Group’s net debt totaled €419.8 million, versus €663.9 million on September 30, 2021, and €979.9 million on March 31, 2021. Adjusted for IFRS 16, net debt totals €256.3 million versus €501.7 million on September 30, 2021, and €807.0 million on March 31, 2021.

Accordingly, the Net debt / EBITDA (ex-IFRS 16) rate calculated over 12 months reached 0.8x as of March 31, 2022. As a reminder, this ratio was 8.8x as of September 30, 2021, while the EBITDA over 12 months was negative on March 31, 2021.

Outlook for the remainder of financial year 2021/2022 revised upward

The spring-summer season is looking good for our leisure parks and ski areas alike. At the same time, the Group remains vigilant in the face of the macroeconomic context, which has become somewhat tense over the last few weeks (due to the impact of inflation, slower growth, and higher costs).

- Sales and EBITDA

- Net Industrial Investments

- Financial gearing

Post-yearend closing event

- Buyout bid on Musée Grévin S.A.

Consequently, and in accordance with the intention Compagnie des Alpes disclosed when the Offer was submitted, and as indicated in the AMF notice published on April 1, 2022, this mandatory squeeze-out of Musée Grévin shares occurred on April 12, 2022 on all Musée Grévin S.A. shares targeted by the Offer that had not been tendered. Since this date, Compagnie des Alpes thus owns 100% of the shares of the Musée Grévin S.A. company.

This press release contains forward-looking statements concerning the prospects and growth strategies of Compagnie des Alpes and its subsidiaries (the “Group”). These statements include indicators pertaining to the Group's intentions, strategies, growth outlook and operating result trends, financial situation, and cash position. Although these indicators are based on data, assumptions, and estimates that the Group considers to be reasonable, they are subject to many risk factors and uncertainties such that the actual results may differ from those anticipated or induced by these indicators due to a multitude of factors, in particular those described in the documents registered with the Autorité des marchés financiers (AMF), available on the Compagnie des Alpes website (www.compagniedesalpes.com). The forward-looking statements contained in this press release reflects the information given by the Group as of the date of this document. Legal obligations to the contrary notwithstanding, the Group expressly declines any obligation to revise or update these provisional statements in light of new information or future developments.

Upcoming events and releases:

- 2021/2022 3rd quarter sales: Thursday, July 21, 2022, after stock market close

- 2021/2022 4th quarter sales: Thursday, October 20, 2022, after stock market close

- 2021/2022 annual results: Tuesday, December 6, 2022, before stock market open

www.compagniedesalpes.com